Imagine a world where banking is faster, safer, and more secure. Blockchain technology provides that and it’s already changing the banking sector’s identity verification game.

We’re all too familiar with the frustration of lengthy, complicated verification processes and the constant threat of identity theft. But with Blockchain, you can streamline these processes, eliminate vulnerabilities, and empower customers with greater control over their data.

Check out our blog to learn about the uncountable possibilities of blockchain identity verification and explore its benefits, real-world applications, and potential to transform the future of banking.

Components of Blockchain Identity Verification

Companies must thoroughly understand its many components to expand the scope of blockchain technology. Here are some of its components to inform more about this transformative technology:

Decentralized Identity: The decentralized method places control in the hands of the people, in stark contrast to the old structures. Users can control the results of their identity-sharing procedure by selecting which information to share and with whom for how long.

Apart from being entirely transparent and unchangeable, an identity model based on blockchain also eliminates the need for third-party mediators, removing any potential dangers or vulnerabilities associated with centralized structures.

Self-Sovereign Identity: Self-sovereign identification is one of the main features of blockchain identity management. According to the approach, consumers should retain complete control over their identities. It allows people to control, amend, and validate their data independently of a centralized authority or outside middleman.

Since they now choose who and how much to share their information with, the risk of data breaches is minimized with the aid of the blockchain identity solution.

Identity Verification Measures: These models aim to authenticate digital identities. Driven by the fundamentals of cryptography, they include creating keys for each identity to ensure safe communication and access.

Consensus algorithms are used in blockchain identity verification setups to ensure that no single party dominates the verification process, increasing the system’s credibility.

The identity-reliant businesses have observed various advantages of blockchain for identity management, driven by its components.

Benefits of Blockchain Identity Verification

Blockchain identity verification provides an innovative approach, resolving many of the challenges of traditional blockchain digital identity solutions verification techniques. Let’s discuss how it benefits:

Enhanced Security: Due to their centralization, traditional digital identity verification in blockchain systems is susceptible to single points of failure. A hacker’s access could compromise the system as a whole.

Blockchain is decentralized, eliminating single points of failure. Every transaction is encrypted and connected to the one before it.

With cryptographic linkage, unauthorized changes are nearly impossible, as even if one block is tampered with, it will be immediately apparent.

User Control: With centralized blockchain identity solutions, corporations can manage individual data by storing it in separate silos. Blockchain returns this authority to the users.

People can decide when, how, and with whom to reveal their personal information using decentralized identity management systems.

This lowers the possibility of data being improperly handled or exploited by other parties while improving data security and privacy.

Reduced Costs: Verifying one’s identity can be expensive, particularly in finance-related industries. These expenses are exacerbated by paperwork, manual verification procedures, and the infrastructure required to operate centralized databases.

With smart contracts, blockchain uses in business can automate many of these procedures, eliminating the need for middlemen and manual intervention while saving substantial money.

Interoperability: In today’s digital world, people’s digital identities and personal information are frequently dispersed across multiple platforms, each with its verification procedure.

Once validated on one site, a user’s digital identity documents can be utilized across many platforms, thanks to blockchain technology, which can establish a single, interoperable system. This improves user ease while streamlining corporate procedures.

Challenges and Concerns of Blockchain Identity Verification

Blockchain technology can revolutionize identity verification. It’s critical to comprehend the main challenges of adopting blockchain development services for identity verification:

- Scalability

Scalability is one of the main challenges that blockchain technology faces. The time needed to process and validate a transaction on a blockchain grows with its volume. Delays in blockchain identity verification may occur, particularly if the system is widely used.

Solutions like layer two protocols and off-chain transactions are being developed to rectify the issue.

- Privacy Concerns

Blockchain technology improves security, but how private it is will determine how much privacy it delivers. Every action on a public blockchain is accessible to every other user on the network due to transaction transparency, which may jeopardize user privacy.

On the other hand, private blockchains greatly reduce privacy threats by restricting transaction visibility and access to approved participants only.

This controlled transparency is crucial in settings where maintaining secrecy is crucial because it allows blockchain’s security features to be utilized without disclosing private information to the general public.

- Regulatory & Legal Issues

Traditional regulatory systems are challenged by the decentralized nature of blockchain technology. Diverse national perspectives on blockchain technology and its uses have resulted in a disjointed regulatory framework.

Companies wishing to use blockchain technology for online services and identity verification may find navigating this complicated legal landscape challenging.

- Adoption Barriers

Blockchain is viewed with mistrust despite its advantages and technological breakthroughs. Adopting relatively new technology can be challenging for many firms, particularly when it conflicts with long-standing procedures.

Moreover, many may be discouraged from adopting blockchain technology due to the requirement for a standardized framework for blockchain identity management and verification and a total ecosystem redesign.

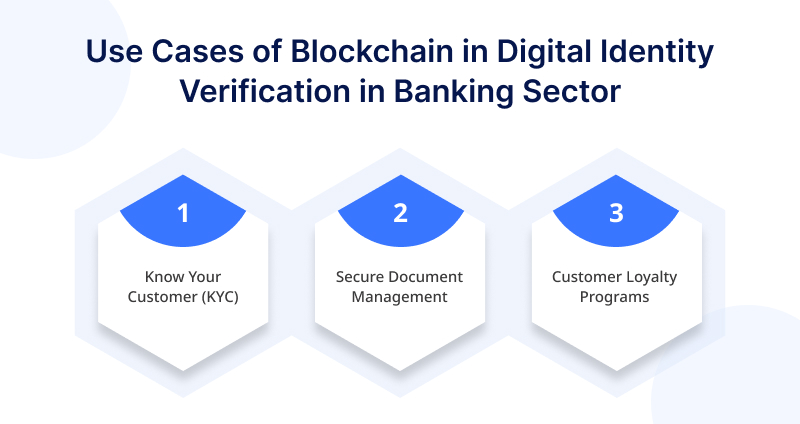

Use Cases of Blockchain in Digital Identity Verification in Banking

Blockchain-driven digital identities can potentially revolutionize a wide range of industries. Here are some compelling use cases of digital identity verification in blockchain within the banking sector:

- Know Your Customer (KYC)

- Blockchain automates KYC/AML, speeding up customer onboarding with real-time identity verification and cost savings.

- A shared blockchain database stores KYC records across banks, ensuring data consistency and eliminating redundancy.

- Blockchain facilitates seamless information exchange between banks, enhancing due diligence and reducing financial crime risks.

- Secure Document Management

- Blockchain securely stores customer documents (e.g., passports, licenses, utility bills), ensuring authenticity and integrity.

- Banks can grant authorized access to specific documents while maintaining overall data security.

- Storing and verifying documents on blockchain streamlines verification and reduces reliance on physical paperwork.

- Customer Loyalty Programs

- Blockchain securely stores loyalty points, rewards, and transaction history, ensuring reliability.

- Banks use blockchain-analyzed customer data to personalize offers and enhance engagement and loyalty.

Future of Blockchain Identity Verification

According to a Market Research Future analysis, the blockchain identity verification market is expected to be valued at 17.81 billion by 2030, with a compound annual growth rate of 56.60% from 2022 to 2030. Increasing governmental initiatives for blockchain technology development in established and emerging countries is expected to aid market expansion.

Due to the continent’s highly advanced infrastructure and technological advancements, North America currently holds the largest market share in the blockchain identity management industry. More and more retailers are searching for methods to improve data security.

One of the few factors propelling this expansion is the growing need for digitalization across various industries, including manufacturing, healthcare, and retail. Blockchain for identity verification systems can efficiently address the growing issue of data leaks and cyberattacks.

Final Words

Blockchain’s revolutionary potential makes banking appear safer, more efficient, and more promising. By utilizing blockchain in app development for identity verification, banks may streamline operations, cut costs, increase customer trust in the financial system, and improve security and preserve client data.

This is about creating a more transparent and safe financial ecosystem and giving customers more control over their data. As we learn more about blockchain’s enormous potential for identity verification, the possibilities appear endless.

Connect with blockchain experts to provide a faster, safer, and more trustworthy banking experience with their digital transformation services.