When buying or selling a home, you might hear the term escrow disbursement and wonder what it means. In real estate transactions, this process plays a crucial role in ensuring funds are handled securely, bills are paid on time, and everyone involved in the deal is protected.

Whether you’re a first-time homebuyer or a seasoned investor, understanding escrow disbursement can help you navigate closing with confidence and avoid unexpected costs. This comprehensive guide breaks down how escrow disbursement works, why it matters, and how it impacts your financial planning.

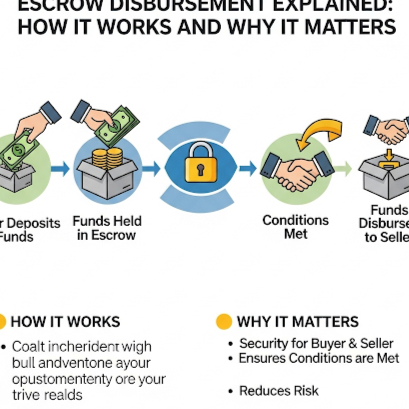

What Is Escrow Disbursement?

Escrow disbursement is the release of funds from an escrow account to pay specific expenses related to a property transaction or ongoing homeownership. These expenses often include:

-

Property taxes

-

Homeowners insurance premiums

-

Mortgage insurance

-

HOA (Homeowners Association) dues

The process ensures that these payments are made on time and in the correct amounts, protecting both the lender and the homeowner from penalties or coverage lapses.

How Escrow Works in Real Estate

When you purchase a property, your lender may require an escrow account. This account acts as a holding place for funds that will be used to pay certain bills related to your home.

Here’s a simplified breakdown:

-

Monthly Contributions – A portion of your monthly mortgage payment goes into your escrow account.

-

Bill Due Dates – When property taxes or insurance premiums come due, your lender uses the funds in escrow to pay them on your behalf.

-

Annual Review – Lenders typically review your escrow account once a year to adjust payments based on changes in tax or insurance costs.

Escrow Disbursement in the Home Buying Process

Escrow disbursement happens at different stages in real estate transactions.

At Closing

When you buy a home, the closing process includes an escrow disbursement to pay for:

-

Seller’s mortgage payoff

-

Agent commissions

-

Property taxes (prorated between buyer and seller)

-

Recording fees and other settlement costs

Example:

John purchased a home for $250,000. At closing, the escrow agent disbursed $200,000 to pay off the seller’s mortgage, $15,000 in agent commissions, and $3,000 for prorated property taxes. The remainder went to the seller.

During Homeownership

Once you own the home, ongoing escrow disbursements ensure your property taxes and insurance are paid on time without you having to remember the due dates.

Example:

Mary’s monthly mortgage payment is $1,500, which includes $250 for escrow. Every six months, her lender uses the funds to pay $1,500 in property taxes directly to the county.

Why Escrow Disbursement Matters

Escrow disbursement isn’t just a formality — it offers real benefits.

Ensures On-Time Payments

By automating tax and insurance payments, you avoid late fees, coverage lapses, or tax liens.

Simplifies Budgeting

Instead of paying large lump sums once or twice a year, escrow allows you to spread these costs evenly across monthly payments.

Protects Lenders and Homeowners

For lenders, escrow ensures the property is properly insured and taxes are current. For homeowners, it provides peace of mind that critical bills are being handled.

The Escrow Disbursement Process Step-by-Step

-

Collection of Funds – The lender collects escrow funds as part of your monthly mortgage payment.

-

Account Monitoring – The escrow account balance is tracked to ensure it meets projected expenses.

-

Bill Receipt – Tax and insurance bills are sent to the lender or escrow company.

-

Disbursement of Funds – The escrow holder releases payment to the relevant party.

-

Annual Analysis – Adjustments are made to account for changes in tax rates or insurance premiums.

Escrow Disbursement Statement

You’ll receive an escrow disbursement statement showing:

-

Amount paid

-

Payment date

-

Recipient (tax authority, insurance company, etc.)

-

Remaining escrow balance

Example:

An annual escrow statement might show $3,200 paid to the county tax collector in January and $1,200 paid to your insurance company in June.

Common Issues with Escrow Disbursement

Even though the process is designed for convenience, problems can arise.

Shortages

If your property taxes or insurance premiums increase unexpectedly, your escrow account may not have enough funds. This can lead to:

-

Higher monthly payments to make up the difference

-

A one-time lump sum request from your lender

Overages

If the bills are lower than expected, you may get a refund or a reduction in monthly payments.

Late Payments

Rarely, administrative errors can cause late payments, leading to penalties or lapses in coverage.

How to Avoid Escrow Disbursement Problems

-

Review your annual escrow analysis closely.

-

Stay informed about property tax and insurance rate changes.

-

Keep your contact information updated with your lender.

-

If you switch insurance companies, notify your lender immediately.

Escrow Disbursement vs. Direct Payment

Some homeowners prefer to pay taxes and insurance directly instead of using escrow.

Advantages of Direct Payment:

-

More control over payment timing

-

Ability to shop for insurance without lender involvement

Disadvantages:

-

Risk of missed payments

-

Need to budget for large, infrequent bills

Real-Life Case Study: Smooth Closing with Escrow Disbursement

James and Linda bought their first home in Texas. Their lender required an escrow account to cover property taxes and insurance. At closing, the escrow officer disbursed funds to the seller’s lender, the title company, and the county tax office. Over the next year, their monthly mortgage payments included escrow contributions, which were later used to pay $5,200 in property taxes and $1,800 in insurance premiums — all without James and Linda lifting a finger.

Escrow Disbursement in Refinancing

When refinancing, a new escrow account may be set up with the new lender. The previous account’s balance is refunded to you, which you can use to fund the new account. Timing these disbursements properly can help avoid gaps in coverage.

Role of Escrow Agents

Escrow agents — whether part of a title company, law firm, or lender — are responsible for:

-

Holding funds securely

-

Making payments as scheduled

-

Keeping accurate transaction records

Their neutral role helps prevent disputes and ensures compliance with contract terms.

Using Escrow Disbursement for HOA Fees

In some cases, escrow disbursement can also cover HOA dues. This is more common in planned communities where fees are predictable and billed regularly.

Best Practices for Homeowners

-

Keep copies of all tax and insurance bills for reference.

-

Review escrow statements annually for accuracy.

-

Contact your lender if you notice discrepancies in disbursement amounts or dates.

Frequently Asked Questions

1. What is an escrow disbursement?

It’s the release of funds from an escrow account to pay property-related expenses like taxes and insurance.

2. Who controls the escrow account?

Your lender or a designated escrow agent manages the account and makes payments on your behalf.

3. Can I stop using escrow?

Some lenders allow it if you have significant equity and a strong payment history, but requirements vary.

4. What happens if there’s not enough money in my escrow account?

Your lender may increase your monthly payments or request a lump sum to cover the shortage.

5. Are escrow disbursements tax-deductible?

While the payments for taxes and mortgage interest may be deductible, the escrow process itself is not.

6. How often do escrow disbursements happen?

It depends on the billing cycles of your tax authority and insurance company — usually annually or semiannually.